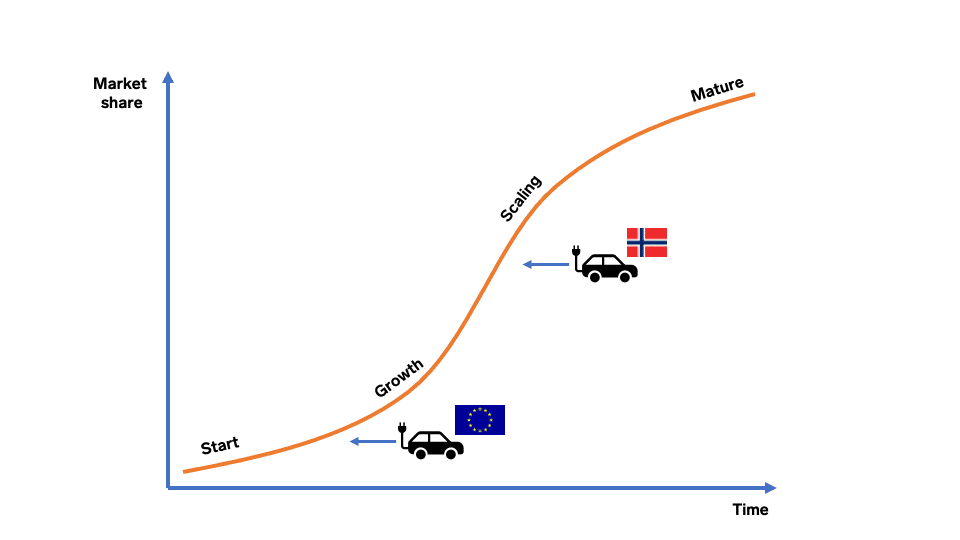

Where is Europe in comparison to Norway in electromobility?

Future exists for electric cars. In Norway, fuel cars are already a thing of the past since the most sold cars are already full-electric ones and the charging infrastructure is in good order. I had a call with my friend and colleague Nina Pavón who lives up in Trondheim, Norway, and works as an investor relations lead at Gofore. As said, Norway is currently estimated to be 5–10 years ahead of the rest of Europe in the electric vehicle (“EV”) market. But what does this mean in practice?

According to Nina, a Tesla driver herself says that choosing an electric car was an easy decision in Norway, the benefits are just too good. This means for instance no road tolls, no car tax, and cheap energy. One of the biggest concerns for novices is obviously charging – how long does it take, where to charge, how do the chargers’ work. In Nina’s case, charging has been well integrated into normal, day-to-day living. This means leaving the car to charge while her son is at football practice, or while shopping for groceries. Chargers are everywhere, and there are many of them. For example, there are fields with 15-20 fast charging points or Tesla superchargers where you always can get your car sufficiently charged in 30 minutes. Many people also charge their cars at home, so the charging happens during the night. The question of range anxiety (in Norwegian: “Rekkeviddeangst”) and other doubts have already been eliminated in Norway (and they do have colder winters than we do in Central-Europe), electric cars are the de facto choice. This is also backed by the numbers because more than 80 % of all cars sold are currently either battery electric vehicles (“BEV”) or plug-in hybrid vehicles (“PHEV”). But how about the rest of us here in Europe, where are we on this? Here are five things you should know:

1. The market is still in an immature phase

Regarding the electromobility market in Europe, the hype is stronger than reality. This goes at least for my bubble. The total amount of electric cars (hybrid and full-electric) in circulation at the end of 2020 was around 1,5% of the total fleet. Naturally, with these kinds of numbers, it is still exceedingly difficult for different market players to make much profit. This also is a chicken-and-egg problem where for example a lot more charging infrastructure is needed to convince people to change to EVs. The other problem also lies in the perceived pricing. Most electric cars still feel economically out of reach for the masses even though the total cost of ownership of an electric car is lower than a traditional car.

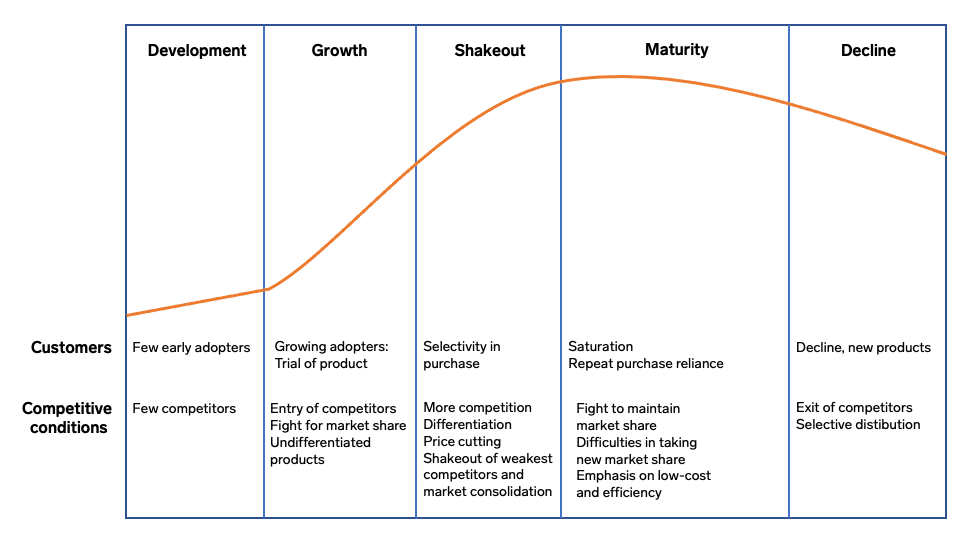

However, being active in this market phase is crucial. Early movers, especially with a customer experience and brand focus, have better possibilities to capture more market share. From a market life cycle model perspective, it is quite easy to see however that we are still in a development phase, but about to enter the growth phase. Giants in the automotive industry are now awake as for example Volkswagen has announced its plans for electromobility with EUR 50 billion investments.

Image 1. Life cycle – adapted from Whittington, Scholes et al.

Image 1. Life cycle – adapted from Whittington, Scholes, et al.

2. The growth is strong and is getting stronger

Even though the adoption level of EVs is still quite low, more importantly as an indicator, there is extraordinarily robust growth on several fronts. In the field of electromobility, a key thing is of course the amount of EVs sold, which in Europe grew by 137% compared to the previous year but still totaled “merely” EUR 1.4 million. What is however interesting is that for instance in Germany the number of electric vehicles tripled in the month of February compared to last year. Regarding the cars, it is obvious that there are many new models that are hitting various kinds of sweet spots for the consumers. Also, the technologies are evolving, for example, the capacity of the batteries are increasing steadily.

Another piece of the puzzle is the public charging infrastructure which has during the last few years grown around 35% per year in Europe. The growth rate around home chargers can be assumed to follow this same pattern. However, this pace will not be enough, and we can also expect the amount of charging stations to increase rapidly. Another thing to consider is the increase in quality and speed of the charging with companies competing over. At least technically. The truth however is that there are still too many slow 22kW chargers out there.

The three main blockers for EV adoption are purchasing price, driving range, and charging infrastructure. The growth is ensuring that these blockers are now being removed very rapidly.

3. The user experience needs development

Like in many other fields there is a lot of variation in the user experiences around e-mobility. Even though some leading manufacturers like Tesla can provide top-notch user experiences in their own charging networks, the chance of finding a non-functioning charger can still be high, or that the charging speed does not fit the user’s current use case. There is also lots of lack of interoperability in the charging standards and one needs to have a stack of different customer cards for the different operators and e.g., contactless card payment is not possible. In my view, this is because many of the parties in the field are still maturing and few end-to-end solutions designed with the end-users in mind do not yet exist. Tesla might be the expectation here, but they are not perfect either. However, we have seen that many other companies, especially those that have tight customer dialogue, are rapidly improving.

Another interesting aspect about the user experience is definitive that it works also the other way around. With this, I mean that companies need to provide these services to their customers in order to provide a holistic user experience. For example, customers with electric cars will prioritize the supermarket or restaurant with a charging possibility available. For more information, we were featured in an article about the customer journey in charging stations.

4. 4. There are still a lot of misconceptions and biases

A recent survey stated that more than half of respondents in the Lower-Saxony area would not be willing to buy an electric car as their next car. For example, 57% of the respondents doubted the environmental friendliness of electric vehicles which can be considered a quite high number. There is no question that electric cars would not be more environmentally friendly than other drive trains. This has been stated in multiple studies.

The other reason included for example the classical driving range issue. It is of course true that few electric cars can reach the same ranges as internal combustion engine cars, but that is the wrong place to compare. A better comparison is how much one needs to drive. According to European statistics, the average daily drive is less than 40 kilometers (pre-covid numbers) and long-distance driving is unusual. EVs are more than good enough in handling the daily needs since in many cases the charging will take place at home or in the context of some other activity like shopping. Many more misconceptions are existing, for example, that the battery will depreciate like in a cell phone and needs to be replaced every two years. The news climate also tends to be such where negative headlines get more clicks. We need to keep on talking about these topics to relentlessly educate and train the market. Not least ourselves.

5. New business models are being unlocked

For me as a professional living and breathing digital transformation, the most exciting thing is the software side and what that is currently unlocking around e-mobility business models. This extends for example to the billing of electricity where we are seeing some variations in form of time-based-, kWh based-, hybrid- or even honey-pot pricing where the energy can even be free or deducted when bundled with other services like in the monthly fee of the car itself or as a part of another service provider. We do not know which pricing model will win the game or will exist at the same time depending on the use case at hand or even customer preferences and needs. Much business model testing is still needed.

The cars themselves are getting new capabilities to change the business models. For example, function-based pricing is something quite exciting. This means that the customer can pay for certain functions such as speed or autonomous-driving features. For example, Audi is already a front-runner with their “on-demand” capabilities. There is still room for a lot of new innovations, and those will be achieved mostly by better software solutions.

Where are we?

As Nina’s experiences showcase, and as the other presented evidence suggests, Norway is leading the way in the EV market. Many of the things we are struggling with, in especially central Europe, are already solved there. What is good is that we can learn quite much about how the market will evolve and how the behavior of people will evolve. Electric mobility will be the new normal and a way of life. The journey has just started, but we are on our way! What are your thoughts on this? Have you tried an electric car already?

Are you interested in this topic? Read also our Case Virta: Accelerating the switch to electric cars